Imagine trying to buy a coffee with Bitcoin in Bogotá. You open your wallet, scan the QR code, and wait. But instead of a simple transaction, you hit a wall built by regulators. In Colombia is a South American country where traditional banks are strictly prohibited from handling cryptocurrency transactions. This isn't just a minor inconvenience; it’s a comprehensive banking ban on crypto activities imposed by the financial watchdogs. If you’re looking to trade, invest, or simply hold digital assets while using Colombian banks, the rules are tight, confusing, and constantly evolving.

You might think that because you can still download an exchange app, everything is fine. But the reality is more complex. The Financial Superintendency of Colombia (SFC) is the regulatory body responsible for overseeing financial institutions and enforcing bans on crypto custody and trading facilitation. has drawn a hard line in the sand. Traditional banks cannot touch crypto. They can’t hold it, they can’t invest in it, and they certainly can’t help you move it. This creates a unique "gray area" where crypto exists legally, but the plumbing of the traditional banking system refuses to connect to it.

The Core of the Ban: What Banks Can and Cannot Do

To understand why your bank account might get flagged or why certain transfers fail, you need to look at the specific restrictions. The SFC didn’t just send a vague memo; they issued detailed external circulars that effectively shut the door on crypto within traditional banking halls.

Here is what the ban actually covers:

- No Custody: Banks cannot hold private keys or store cryptocurrencies on behalf of clients.

- No Investment Products: You won’t find ETFs or mutual funds backed by Bitcoin offered by standard Colombian banks.

- No Facilitation: Banks cannot use their platforms to process transactions involving digital assets. This means if you try to wire money to a known crypto exchange, the bank’s compliance software will likely block it.

This restriction applies to all supervised financial entities. It’s not just about big names like Bancolombia is Colombia's largest bank which navigated regulations by launching its own separate crypto platform called Wenia.; it affects every smaller regional bank too. The goal? To prevent money laundering and protect the autonomy of the Central Bank. But for the average user, it means being pushed out of the comfortable ecosystem of online banking and into the wilder west of fintech apps and peer-to-peer networks.

The $150 Threshold: How Reporting Works

If banks are off the table, how does money move? Enter the Payment Service Providers (PSPs) and Virtual Asset Service Providers (VASPs). These companies operate in a different lane, but they come with heavy surveillance. The Financial Information and Analysis Unit (UIAF) is Colombia's financial intelligence unit that monitors suspicious transactions and receives reports from crypto businesses. is watching closely.

Here is the rule that catches most people off guard: any crypto transaction exceeding USD 150 triggers mandatory reporting. That’s right. If you swap coins, deposit fiat, or withdraw funds above this tiny threshold, the PSP must capture full sender and recipient data. They aren’t just checking boxes; they are submitting suspicious transaction reports in real-time if anything looks odd.

This low threshold was designed to catch illicit flows early. For legitimate users, it means your privacy is significantly reduced. Every time you move more than $150 worth of crypto, you are leaving a digital footprint that goes straight to government analysts. Fines for non-compliance are steep-some PSPs have faced penalties topping USD 1.5 million. As a result, these companies are aggressive about Know Your Customer (KYC) checks. Expect lengthy verification processes before you can even make your first trade.

| Country | Banking Access | Key Regulatory Feature | Stablecoin Status |

|---|---|---|---|

| Colombia | Banned for traditional banks | SFC restrictions + UIAF reporting ($150 limit) | COPW launched by Bancolombia |

| Brazil | Open | Comprehensive tax law effective Jan 2025 | Regulated under payment laws |

| Chile | Open | Approved digital asset custodians in 2025 | Unrestricted usage |

| Argentina | Limited | Bitcoin accepted for international trade | High inflation drives adoption |

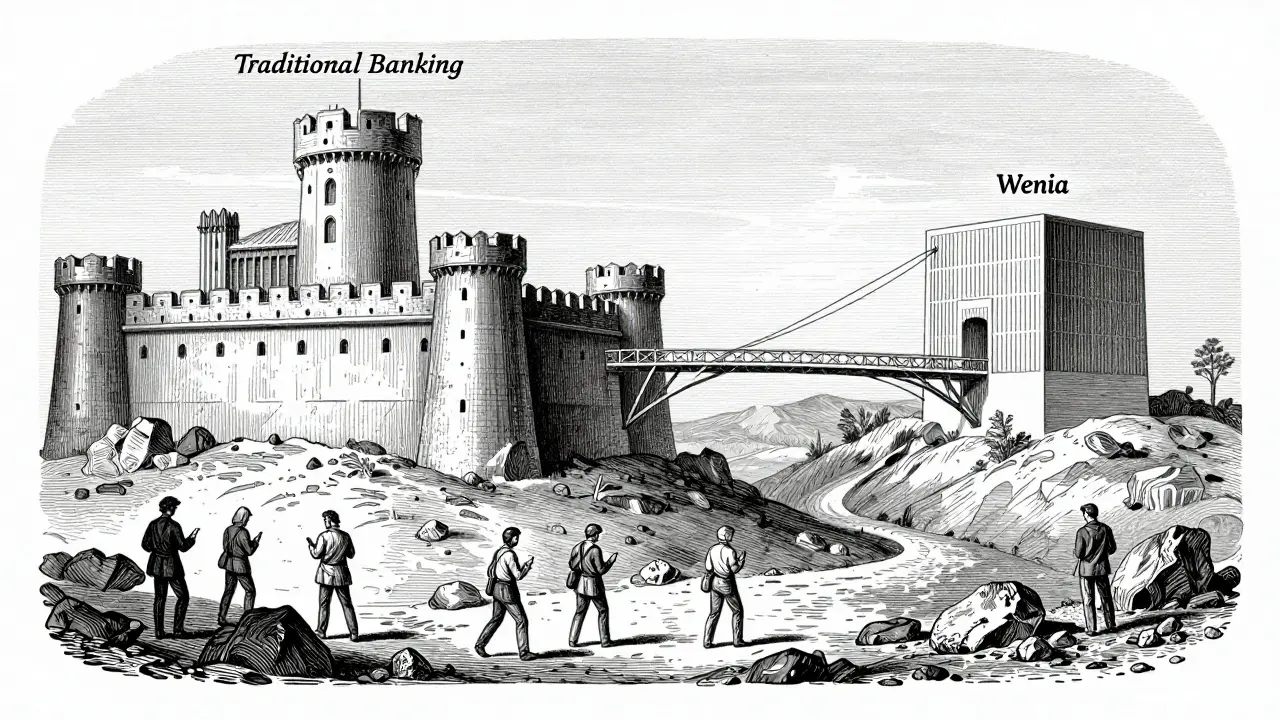

The Bancolombia Paradox: Innovation Within Restrictions

So, if banks can’t touch crypto, how did Bancolombia launch Wenia is a cryptocurrency exchange platform launched by Bancolombia to offer regulated crypto services to its customers.? And what about the COPW Stablecoin is a digital currency pegged to the Colombian Peso, created to facilitate faster and cheaper domestic payments.? This seems contradictory, doesn’t it?

It’s not a contradiction; it’s a loophole exploited by giants. The SFC banned *traditional* banking functions from mixing with crypto. It didn’t ban banks from creating *separate* legal entities to do it. Bancolombia spun off Wenia as a distinct operation. By doing so, they kept their core banking license clean while still offering crypto services to their massive customer base. COPW works similarly-it’s a tool for efficiency, not speculation, aimed at settling payments instantly without touching the traditional interbank clearing systems.

This model signals that institutional support is strong, but only for those who can afford the compliance overhead. For the rest of us, it highlights the gap between the elite financial sector and the everyday user. While Bancolombia users might get smoother integration, independent traders are left navigating the choppy waters of third-party exchanges and strict UIAF oversight.

Regional Context: Why Colombia Is Different

Look south, and the picture changes. In 2024, Brazil passed clear crypto tax laws. Chile approved dedicated custodians. Even Argentina, despite its economic turmoil, recognized Bitcoin for international trade. Colombia sits in the middle-not banning crypto outright (like some countries did), but making it incredibly difficult to interact with via traditional finance.

Why this hesitation? Minister of Finance Ricardo Bonilla has stated that crypto operations must be reviewed to ensure no threat to the Central Bank’s authority. He acknowledges crypto is a "reality," but insists on control. The fear is twofold: loss of monetary sovereignty and increased risk of financial crime. Compared to neighbors, Colombia’s approach is cautious, almost defensive. It prioritizes stability over innovation, forcing the market to adapt rather than welcoming it with open arms.

Navigating the Gray Area: Practical Steps for Users

If you live in Colombia and want to engage with crypto, you have to play by these new rules. Here is how to stay compliant and avoid headaches:

- Use Regulated Exchanges: Stick to platforms that are registered with the UIAF. Unregistered offshore exchanges might seem attractive, but if things go wrong, you have zero recourse. Plus, moving money to them becomes nearly impossible due to bank blocks.

- Expect Friction: Don’t expect instant deposits. Your PSP will verify your identity, source of funds, and purpose of transaction. Keep documentation handy.

- Watch the Thresholds: Remember the $150 rule. If you’re moving small amounts frequently, structure your transactions carefully, but never attempt to break them up solely to evade reporting-that’s structuring, and it’s illegal.

- Tax Compliance: The DIAN (tax authority) treats crypto as intangible assets. Capital gains are taxable. Keep records of every trade. Ignorance is not a defense when auditors come knocking.

- Avoid Bank Transfers to Exchanges: Direct wires from your main bank account to a crypto exchange will likely be rejected. Use specialized fintech payment rails or prepaid cards designed for this purpose.

The landscape is shifting. The original SFC regulatory sandbox expired in December 2023, leaving some uncertainty for new business models. However, the pressure for clarity is mounting. With global standards tightening and local demand growing, expect updates. Until then, proceed with caution, document everything, and assume that every transaction is being watched.

Is cryptocurrency illegal in Colombia?

No, owning and trading cryptocurrency is not illegal in Colombia. However, traditional banks are prohibited from facilitating these transactions, holding custody, or offering crypto investment products. You can still buy and sell crypto through licensed exchanges and fintech apps, but you must comply with strict reporting rules.

Why did my bank block my transfer to a crypto exchange?

Colombian banks are explicitly forbidden by the Financial Superintendency of Colombia (SFC) from processing transactions involving cryptoassets. If your bank identifies that the recipient is a crypto-related entity, they are required to block the transfer to remain compliant with anti-money laundering regulations.

What happens if I transact more than $150 in crypto?

Transactions exceeding USD 150 trigger mandatory reporting to the UIAF. The payment service provider must collect full details about the sender and receiver. This is not a penalty for you, but it means your activity is monitored more closely. Ensure your KYC information is accurate to avoid delays.

Can I use Bancolombia to buy Bitcoin directly?

You cannot buy Bitcoin directly through the traditional Bancolombia banking app. However, Bancolombia offers a separate platform called Wenia, which is a regulated crypto exchange. You can link your accounts, but the services are segregated to comply with SFC restrictions on traditional banking functions.

Do I have to pay taxes on my crypto profits?

Yes. The Colombian tax authority (DIAN) considers cryptocurrencies as intangible assets. Any capital gains realized from selling crypto are subject to personal or corporate income tax. You must report these gains in your annual tax declaration.