Imagine checking your wallet balance on January 2, 2025, and realizing that every satoshi you hold is now a taxable event waiting to happen. For years, the status of cryptocurrency in Russia was a legal gray zone where users operated with uncertainty about potential liabilities. That ambiguity ended abruptly. With the implementation of Federal Law No. 418-FZ is the legislative framework establishing cryptocurrency as taxable property effective January 1, 2025, the government has drawn a clear line in the sand. If you are holding digital assets or running a mining rig in the Russian Federation, the rules have changed fundamentally.

This isn't just about filling out a form. It’s about navigating a complex web of income thresholds, regional bans, and strict reporting requirements designed by the Federal Tax Service (FTS) is the government agency responsible for collecting taxes and monitoring compliance with fiscal laws. Whether you are a casual investor who bought Bitcoin during a dip or a corporate entity managing large-scale mining operations, understanding these new obligations is critical to avoiding heavy fines.

How Individual Income Tax Works for Crypto

The most immediate change for retail investors involves how personal income from cryptocurrency is calculated. Under Article 210, Clause 2.1, Paragraph 8.3 of the Russian Tax Code is the comprehensive set of laws governing tax collection and obligations in Russia, your crypto gains are no longer treated in isolation. They are consolidated with your income from securities transactions. This means if you made money selling stocks and also sold Ethereum, those amounts are added together to determine your tax bracket.

For residents, the system uses a progressive rate structure:

- 13% Personal Income Tax (PIT): This applies if your total annual income from crypto and securities does not exceed 2.4 million rubles (approximately $32,653 at current exchange rates).

- 15% Personal Income Tax (PIT): This higher rate kicks in for any amount exceeding the 2.4 million ruble threshold.

If you are a non-resident working in Russia or earning from within the country, the rules are stricter. You face a flat 30% tax rate on all cryptocurrency income, regardless of the amount. There is no threshold exemption for non-residents.

A crucial detail often overlooked is the lack of an ownership period exemption. Unlike other movable property, which might be tax-free after three years of holding, cryptocurrency requires tax payment upon sale regardless of how long you held it. As confirmed by legal analyst Sergey Tereshkin in early 2025, this eliminates the "buy and hold" tax shelter strategy for digital assets.

Corporate Mining and Business Obligations

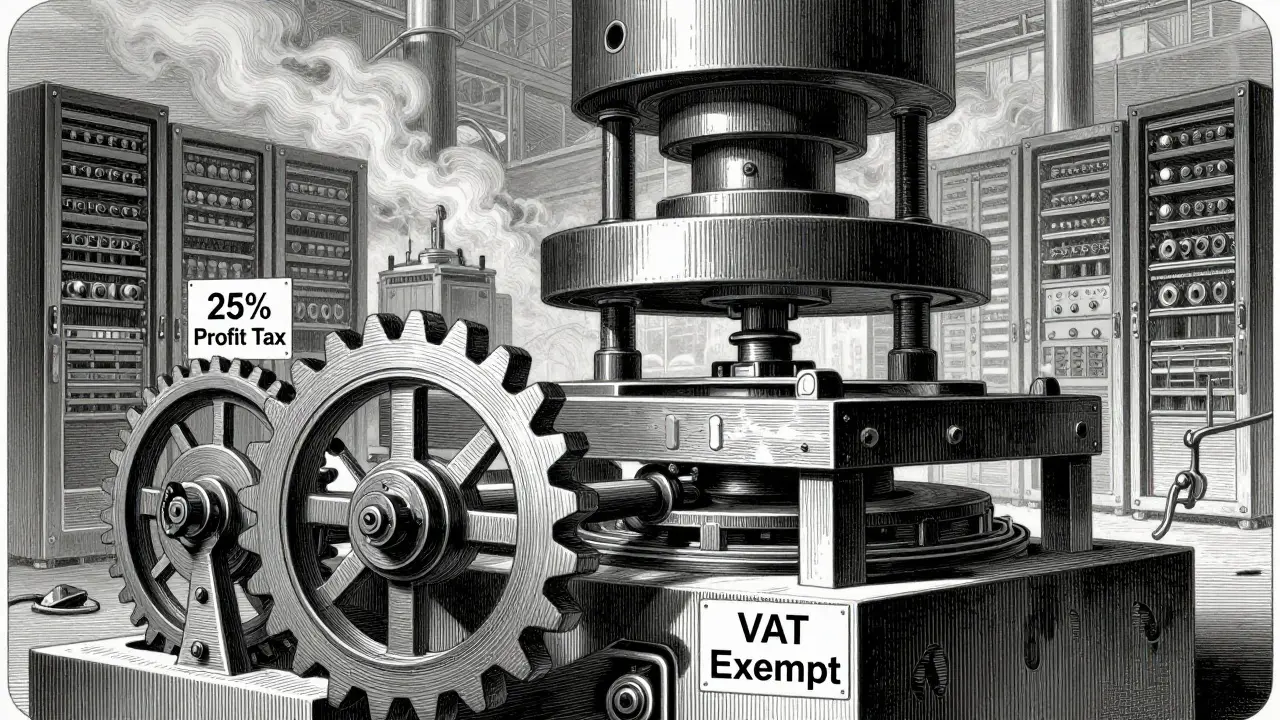

Running a mining operation in Russia is significantly more regulated than simply holding tokens. The law mandates that all corporate entities involved in mining or selling cryptocurrency must use the General Taxation System (OSNO). This prohibits businesses from using simplified tax regimes like USN (Simplified Taxation System) or AUSN (Automatized Simplified Taxation System), which many small tech startups previously relied on.

The tax burden for corporations is substantial:

- 25% Profit Tax: This applies to profits generated from mining operations and cryptocurrency sales. Note that this is 20% higher than the standard profit tax rate for many other industries.

- Mandatory VAT Exemption: While the profit tax is high, transactions involving cryptocurrency are exempt from Value-Added Tax (VAT). This was a key recommendation from the Ministry of Finance's working group to prevent double taxation and align with international practices.

Calculating the tax base for corporations is not straightforward. You cannot simply pick the price from any random exchange. According to Article 282.3 of the Tax Code, you must use market quotations from foreign trading organizers that meet specific criteria: they must have a daily trading volume exceeding 100 billion rubles and provide publicly available quotation data for at least three years. This requirement aims to ensure price transparency but adds complexity to accounting processes.

| Participant Type | Tax Rate | Threshold / Condition | Special Regimes Allowed? |

|---|---|---|---|

| Individual Resident | 13% or 15% | Progressive based on 2.4M RUB limit | No (Standard PIT) |

| Non-Resident | 30% | Flat rate on all income | No |

| Corporate Entity | 25% | On net profit from mining/sales | No (Must use OSNO) |

Geographic Restrictions and Mining Bans

Taxation is only half the story; physical restrictions play a major role in who can mine where. The government has implemented strict geographic limitations on mining activities to manage energy loads and regulatory control.

As of 2025, mining operations are completely prohibited in the following regions until at least 2031:

- Dagestan

- Chechnya

- Donetsk People's Republic (DPR)

- Luhansk People's Republic (LPR)

In other energy-intensive regions, such as Irkutsk Oblast, Buryatia, and Zabaykalsky Krai, mining faces seasonal restrictions. During periods of energy deficit, typically winter months, operators may be forced to shut down or reduce capacity. These restrictions have led to a 22% decline in domestic mining operations in Irkutsk since the start of 2025, according to Central Bank reports.

Reporting Requirements and Penalties

The Federal Tax Service has established dedicated channels for digital asset reporting. Compliance is not optional, and the penalties for non-compliance are severe.

You are required to file quarterly reports detailing your cryptocurrency holdings and transactions. Failure to submit these reports can result in fines up to 40,000 rubles per violation. If you fail to pay the assessed tax, the penalties escalate to 15-40% of the unpaid amount, plus accrued interest.

Record-keeping is another significant hurdle. The FTS guidance issued in January 2025 requires taxpayers to maintain detailed records of:

- Wallet addresses used for transactions

- Transaction IDs (hashes)

- Exchange rates at the exact time of each transaction

Many accounting firms reported needing specialized training to handle these calculations. A survey by Acsour found that 89% of firms needed 2-3 weeks of staff training to adapt to the new crypto tax calculation methods. The primary difficulty cited was verifying foreign exchange quotations due to the absence of domestic regulated exchanges.

Market Impact and User Reactions

The introduction of these rules has had a tangible impact on the market. In November 2024, immediately following the announcement of the law, there was an 8% spike in exchange traffic as users rushed to understand their positions. However, by Q1 2025, the number of active users dropped from 1.8 million to 1.4 million.

Why the drop? Many small investors are migrating to peer-to-peer (P2P) platforms to avoid reporting thresholds. Pavel Zryachikh, CEO of Garantex, noted that 78% of his user base had annual transaction volumes below the 600,000 ruble ($8,163) reporting threshold, suggesting the regulations disproportionately affect smaller players while pushing activity underground.

Conversely, institutional participation has risen. By late February 2025, 47 traditional financial institutions registered as cryptocurrency service providers. The clarity provided by the VAT exemption and defined tax rates has attracted larger entities willing to navigate the compliance costs.

What Comes Next?

The regulatory landscape is still evolving. The State Duma is scheduled to debate amendments to Federal Law No. 418-FZ in July 2025, focusing specifically on clarifying the 600,000 ruble annual reporting threshold. Current ambiguities leave many users unsure whether multiple small transactions trigger mandatory reporting.

Additionally, the integration with the experimental legal regime for cross-border cryptocurrency transactions (Presidential Decree No. 123) offers unique opportunities for international trade settlements, particularly in navigating Western sanctions. The Ministry of Finance projects crypto-related tax revenue to reach 12 billion rubles in 2025, growing to 28 billion rubles by 2027. However, independent analysts suggest these figures may be overestimated by 30-40% due to ongoing market contraction among retail users.

Is cryptocurrency considered legal property in Russia?

Yes. Since January 1, 2025, under Federal Law No. 418-FZ, cryptocurrency is formally recognized as property for tax purposes. This legal recognition allows individuals and companies to own and transact with digital assets, provided they comply with tax and reporting obligations.

Do I need to pay tax if I hold crypto for more than three years?

Yes. Unlike other movable property, cryptocurrency does not qualify for the three-year ownership exemption. You must pay personal income tax on gains when you sell or transfer crypto, regardless of how long you have held it.

Where is crypto mining banned in Russia?

Mining is completely prohibited in Dagestan, Chechnya, and the DPR/LPR territories until 2031. In Irkutsk Oblast, Buryatia, and Zabaykalsky Krai, mining faces seasonal restrictions during energy deficit periods.

What is the tax rate for corporate crypto mining?

Corporate entities must pay a 25% profit tax on income from mining and sales. They are required to use the General Taxation System (OSNO) and cannot utilize simplified tax regimes. However, these transactions are exempt from VAT.

How do I calculate the value of my crypto for tax purposes?

You must use market quotations from foreign trading organizers that meet specific criteria: daily trading volume over 100 billion rubles and three years of public quotation data. You cannot use prices from unregulated local exchanges.

What are the penalties for failing to report crypto income?

Failure to submit quarterly reports can result in fines up to 40,000 rubles. Non-payment of assessed taxes triggers penalties of 15-40% of the unpaid amount, plus interest. Detailed record-keeping of wallet addresses and transaction IDs is mandatory.

seriously the government is just trying to squeeze every last ruble out of us while the grid collapses in irkutsk. its a total scam and anyone who thinks this makes sense is delusional. we need to fight back against these oppressive regulations immediately.

i totally get why people are frustrated lorna. it feels like they are punishing regular folks for trying to save money or invest in something new. maybe we can find some ways to help each other navigate this without getting fined too much?

oh please spare me the tears. you people are so naive thinking the state cares about your little bitcoin bags. this is exactly what happens when you let unregulated tech run wild without proper oversight. the moral decay of society is evident in how everyone ignores basic fiscal responsibility. typical.

its wild to think about how the tax code now treats crypto gains just like stock sales but with way more red tape. i wonder if the progressive rate structure will actually catch small investors or if it mostly hits the whales who move millions around. the whole system seems designed to create chaos rather than clarity.

im so confused abt the reporting part lol. do i really have to keep track of every single transaction hash? that sounds like a nightmare for my brain. hope someone figures out an easy way to do this bc im not gonna pay 40k rubles for forgetting to file a form.

stop complaining and start adapting. the rules are clear if you read them. non-residents pay 30% flat period. residents pay 13-15%. just do the math and pay up. weak minds look for excuses strong minds find solutions.

hey diana chill out a bit. rosie has a point its super complicated especially with the foreign exchange quotation requirements. maybe we can share some tips on which exchanges meet the criteria so everyone stays safe from fines. lets help each other out instead of yelling.