When you hear the word blockchain, your mind probably jumps to Bitcoin prices or the latest crypto trend. But the technology behind it has a much deeper, stranger, and more fascinating backstory. It didn't start in a Silicon Valley garage with a plan to disrupt Wall Street. It started as a theoretical solution to a problem no one really cared about yet: how to prove when a digital document was created without trusting anyone.

To understand where we are today-with billions locked in decentralized finance and NFTs selling for millions-we have to rewind. We need to look at the cryptographers, the failed experiments, and the accidental breakthroughs that turned a niche academic concept into global infrastructure. This isn’t just a timeline; it’s a story of how trust was digitized.

The Pre-Bitcoin Era: Laying the Cryptographic Groundwork

Long before Satoshi Nakamoto appeared on the internet, researchers were already trying to solve the "double-spending" problem-how to ensure digital money can’t be copied and spent twice. In 1982, cryptographer David Chaum published his dissertation titled "Computer Systems Established, Maintained, and Trusted by Mutually Suspicious Groups." He proposed a system for anonymous electronic cash. It was brilliant, but it relied on a central authority to manage the transactions. That central point of failure would eventually become the Achilles' heel of early digital currency attempts.

The real spark for modern blockchain came in 1991. Stuart Haber and W. Scott Stornetta, working for the US software company Bellcore, wanted to prevent the backdating of documents. They developed a computationally secure chain of blocks linked together using cryptography. Each block contained a timestamp and a hash of the previous block. If you tried to change an earlier document, the hash would change, breaking the chain and alerting everyone to the tampering.

In 1992, they improved this design by adding Merkle trees. This allowed multiple document certificates to be gathered into a single block, making the process much more efficient. Their company, Surety, even published these document certificate hashes in The New York Times every week starting in 1995. Yes, the New York Times helped validate early blockchain-like records. It’s a humble beginning for a technology that now challenges central banks.

Other pioneers chipped in during the late 90s and early 2000s. Nick Szabo proposed "b-money" in 1998, a decentralized digital currency system that never got off the ground due to consensus issues. In 2004, Hal Finney introduced "Reusable Proof of Work," a digital cash system that kept ownership records on a trusted server-a step closer to decentralization but still not fully there. Adam Back also implemented Hashcash in 2004, originally designed to combat email spam and DDoS attacks. This proof-of-work mechanism would later become the engine powering Bitcoin mining.

2008-2013: The Birth of Bitcoin and Decentralized Trust

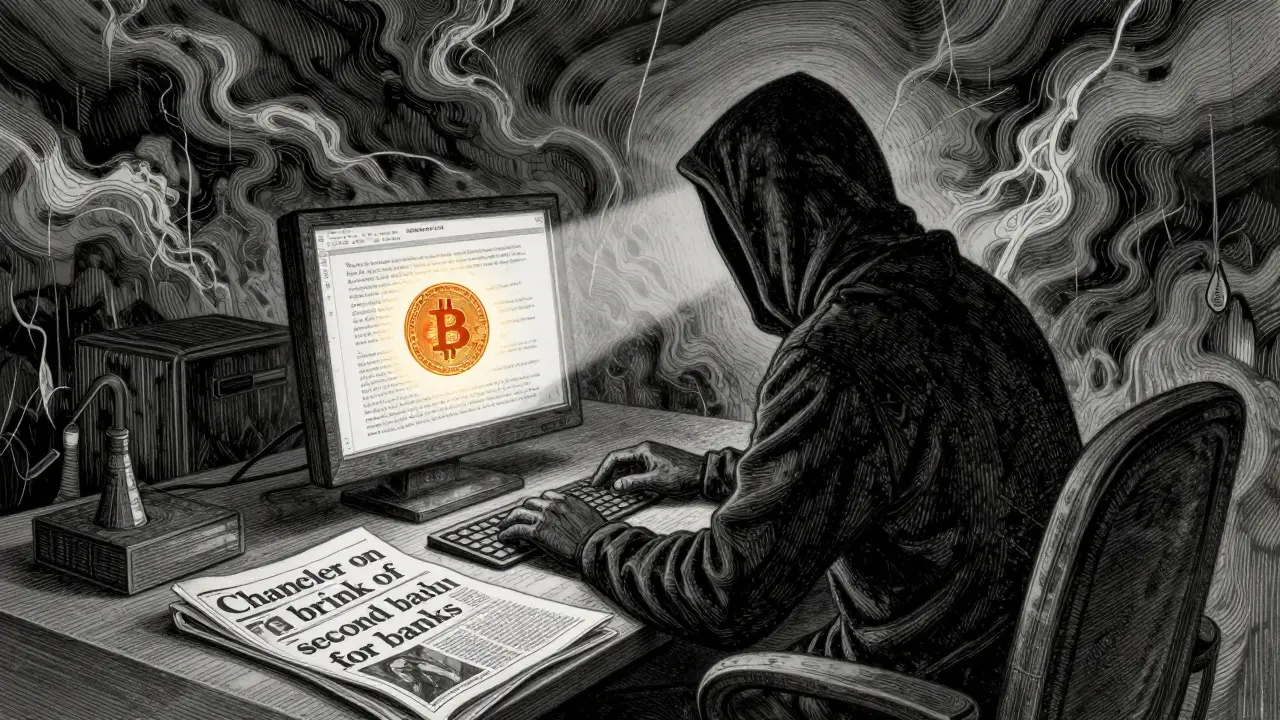

Then came October 31, 2008. Amidst the global financial crisis, a pseudonymous person or group named Satoshi Nakamoto published the Bitcoin whitepaper. The genius wasn’t just in creating a new currency; it was in solving the double-spending problem without a central authority. Nakamoto combined the existing concepts of proof-of-work (from Hashcash) and cryptographic timestamps (from Haber and Stornetta) into a peer-to-peer network.

The Bitcoin network went live in January 2009 with the mining of the "Genesis Block." Inside the block’s data, Nakamoto embedded a headline from The Times newspaper: "Chancellor on brink of second bailout for banks." It was a subtle protest against traditional finance and a permanent timestamp marking the birth of a new era.

For a while, Bitcoin was mostly a curiosity for cypherpunks and computer scientists. Its first real-world transaction happened in May 2010, when a programmer named Laszlo Hanyecz paid 10,000 BTC for two pizzas. At the time, that was worth about $41. Today, those pizzas would be worth hundreds of millions of dollars. This event, known as Bitcoin Pizza Day, remains a favorite anecdote in the community, highlighting both the absurdity and the potential of early adoption.

By 2011, the ecosystem began to diversify. Alternative cryptocurrencies, or "altcoins," like Namecoin and Litecoin emerged. Namecoin aimed to provide a decentralized domain name system, while Litecoin focused on faster transaction times. These projects proved that the underlying blockchain code could be forked and modified for different purposes. By 2013, the total value of all bitcoins had surpassed $1 billion, signaling that this was no longer just a tech experiment-it was becoming an asset class.

2013-2017: Smart Contracts and the Ethereum Revolution

If Bitcoin was version 1.0 of blockchain, Ethereum was version 2.0. In 2013, Vitalik Buterin, a young programmer who had contributed to Bitcoin Magazine, realized that Bitcoin’s scripting language was too limited. He wanted a blockchain that could do more than just move money. He wanted it to run programs.

Buterin proposed Ethereum, introducing the concept of smart contracts. These are self-executing contracts with the terms of the agreement directly written into code. When predetermined conditions are met, the contract executes automatically. This opened the door to Decentralized Applications (DApps). Instead of just being a ledger for money, the blockchain became a global computer.

Ethereum launched in July 2015 after a successful crowdsale in 2014. Almost immediately, it changed the landscape. Developers no longer needed to build their own blockchains for every new idea; they could build on top of Ethereum. This led to an explosion of innovation, but also significant risks.

In 2016, the Dark Army exploited a vulnerability in a project called The DAO (Decentralized Autonomous Organization), stealing $60 million worth of Ether. This hack highlighted the dangers of untested smart contract code. The Ethereum community faced a difficult choice: leave the stolen funds where they were (preserving immutability) or reverse the transaction (preserving user assets). They chose the latter, leading to a hard fork that split the network into Ethereum and Ethereum Classic. It was a messy moment, but it taught the industry a crucial lesson: code is law, but bugs can cost you everything.

Despite the drama, 2017 saw the Initial Coin Offering (ICO) boom. Hundreds of projects raised billions of dollars by selling tokens to investors. While many of these projects were scams or failed startups, the capital influx accelerated development across the entire blockchain sector. Companies like EOS.IO unveiled new protocols designed specifically for high-throughput DApps. The Linux Foundation also launched Hyperledger in 2015, bringing enterprise-grade blockchain development to the table, focusing on permissioned networks for businesses rather than public cryptocurrencies.

2018-Present: Maturation, DeFi, and Interoperability

After the ICO bubble burst in 2018, the market entered a "crypto winter." Prices crashed, and hype died down. But for developers, this was a golden age. With less noise, teams focused on building robust infrastructure. This period marked the transition from speculation to utility.

The rise of Decentralized Finance (DeFi) was the biggest shift. Platforms like Uniswap, Aave, and Compound allowed users to lend, borrow, and trade assets without intermediaries like banks. By 2020, the Total Value Locked (TVL) in DeFi protocols reached billions of dollars. You could earn interest on your crypto or take out loans using your tokens as collateral, all through automated code. This demonstrated that blockchain could actually replicate-and in some cases improve upon-traditional financial services.

At the same time, Non-Fungible Tokens (NFTs) moved from a niche art collector’s item to a mainstream phenomenon. In 2020 and 2021, NFTs revolutionized digital ownership. Artists, musicians, and brands used them to sell unique digital items, proving scarcity in a world where copying files is free. While the market has seen volatility, the underlying technology for verifying digital provenance has found lasting applications in gaming, ticketing, and identity verification.

Scalability remained a major hurdle. As more people used Ethereum, transactions became slow and expensive. The solution arrived in September 2022 with "The Merge." Ethereum transitioned from Proof of Work (mining) to Proof of Stake (staking). This reduced the network’s energy consumption by over 99% and laid the groundwork for future scalability upgrades. It was a monumental technical achievement, proving that large, decentralized networks can evolve without breaking.

Regulation also caught up. In 2022 and 2023, governments worldwide began implementing clearer frameworks for digital assets. The EU’s MiCA regulation and various US agency guidelines provided more certainty for businesses. This didn’t kill innovation; it forced it to mature. Projects had to comply with standards, which filtered out many low-quality actors and brought institutional players into the fold.

Where Do We Go From Here?

We are now in an era defined by interoperability and integration. Early blockchains were isolated silos. Today, bridges and cross-chain protocols allow different networks to communicate. Assets can move between Ethereum, Solana, Polkadot, and others seamlessly. This creates a unified internet of value rather than fragmented islands.

Enterprise adoption is also accelerating. Supply chains use blockchain for transparency, allowing consumers to trace the origin of products from farm to shelf. Central Bank Digital Currencies (CBDCs) are being tested by dozens of countries, exploring how sovereign nations can issue digital fiat currencies on distributed ledgers. And with the rise of AI, we’re seeing experiments in using blockchain to verify the authenticity of AI-generated content and manage data rights.

The journey from Stuart Haber’s timestamped documents to a multi-trillion-dollar decentralized economy is remarkable. Blockchain has evolved from a simple list of records into a complex layer of internet infrastructure. It’s no longer just about replacing banks; it’s about redefining how we establish trust, ownership, and cooperation in a digital world. The next chapter will likely involve invisible integration-where you use blockchain technology daily without even realizing it, just as you use the TCP/IP protocol when browsing the web.

| Year | Milestone | Significance |

|---|---|---|

| 1991 | Haber & Stornetta | First cryptographically secured chain of blocks for timestamping. |

| 2008 | Bitcoin Whitepaper | Satoshi Nakamoto proposes decentralized digital currency. |

| 2009 | Bitcoin Launch | First practical implementation of a decentralized blockchain. |

| 2015 | Ethereum Launch | Introduction of smart contracts and programmable blockchain. |

| 2017 | ICO Boom | Massive capital influx accelerates ecosystem growth. |

| 2020 | DeFi & NFT Rise | Mainstream adoption of decentralized finance and digital ownership. |

| 2022 | Ethereum Merge | Transition to Proof of Stake, reducing energy use by 99%. |

Who invented blockchain technology?

While Satoshi Nakamoto is credited with creating the first decentralized blockchain in 2008 for Bitcoin, the foundational concepts were developed earlier. Stuart Haber and W. Scott Stornetta described the first cryptographically secured chain of blocks in 1991. Other contributors include David Chaum (1982) and Hal Finney (2004).

What is the difference between Bitcoin and Ethereum?

Bitcoin is primarily a decentralized digital currency and store of value. Its blockchain is optimized for secure transactions. Ethereum, launched in 2015, is a programmable blockchain that supports smart contracts and decentralized applications (DApps). This allows developers to build complex systems like DeFi platforms and NFT marketplaces on top of it.

How did blockchain evolve from cryptocurrency to other uses?

The introduction of smart contracts by Ethereum in 2015 was the key turning point. Smart contracts enabled automated agreements without intermediaries, paving the way for Decentralized Finance (DeFi), supply chain tracking, digital identity, and non-fungible tokens (NFTs). This expanded blockchain's utility beyond simple peer-to-peer payments.

What was the significance of the Ethereum Merge in 2022?

The Merge transitioned Ethereum from Proof of Work (mining) to Proof of Stake. This reduced the network's energy consumption by approximately 99%, addressing major environmental concerns. It also laid the foundation for improved scalability and security in future upgrades.

Is blockchain technology only used for cryptocurrency?

No. While cryptocurrency was the first application, blockchain is now used in various industries. Examples include supply chain management for product traceability, healthcare for secure patient records, voting systems for election integrity, and real estate for transparent property transactions.

they say its for trust but i know the truth. it is just a way for the banks to watch us all. they put chips in our phones and now they want chips in our money too. this blockchain stuff is a trap to steal our souls and data. do not buy into it. they are watching you right now reading this. stay away from the digital devil.

you are so wrong about the ny times part. i read somewhere that surety was actually a front for the cia back in the day. also your post has like 5 typos in the first paragraph. did u even proofread this? it makes me sick when people write bad articles about serious tech. i bet you dont even own any crypto yourself or you wouldnt be so naive. typical fake news writer trying to sell ads.

hey there! nice summary of the history here. i think a lot of people forget about hashcash and how adam back helped with spam fighting before bitcoin used it. it is cool to see how things connect. i have been running a node for years and it is pretty stable now. the merge really did help with energy use as stated. hope everyone keeps learning about this tech!

It is imperative that we recognize the underlying surveillance state architecture embedded within these distributed ledgers. The notion of anonymity is a fallacy propagated by those who wish to obscure the panopticon nature of cryptographic tracking. Every transaction is recorded forever, creating an immutable record of your every move for the authorities to access at will. We must remain vigilant against this encroachment on our privacy under the guise of decentralization. The government will inevitably seize control of these networks through regulatory capture.

The article overlooks the significant contributions of Indian researchers in cryptography and blockchain development. While Western narratives dominate, India has produced brilliant minds who have advanced secure communication protocols. It is important to acknowledge global innovation rather than focusing solely on Silicon Valley or European origins. Our nation plays a crucial role in the future of digital infrastructure and should be recognized accordingly in such historical accounts.